Money has always depended on trust.

Whether someone deposits money into a bank, contributes monthly savings to a SACCO, pays an insurance premium, or sends funds across borders, every financial transaction relies on accurate records and confidence that those records have not been altered.

For decades, financial institutions have built increasingly sophisticated systems to manage this trust. Banks invested heavily in secure databases. Payment providers developed real-time settlement systems. Regulators introduced stricter compliance requirements. Insurance companies expanded fraud detection capabilities. Fintech companies created digital platforms that brought financial services closer to customers than ever before.

Yet despite these advances, many challenges remain.

Financial institutions still spend billions of dollars every year reconciling records across disconnected systems. International payments can involve multiple intermediaries before reaching their destination. Identity verification often requires customers to repeatedly submit the same documents. Fraud continues to evolve alongside digital financial services, while regulatory obligations become more demanding each year.

At the same time, customer expectations are changing.

People expect payments to happen instantly. They want secure digital onboarding, transparent financial services, and seamless experiences across mobile apps, online banking platforms, and payment systems. Businesses want faster settlements, lower transaction costs, and greater confidence when exchanging information with other organizations.

This changing environment has placed blockchain at the center of conversations about the future of financial services.

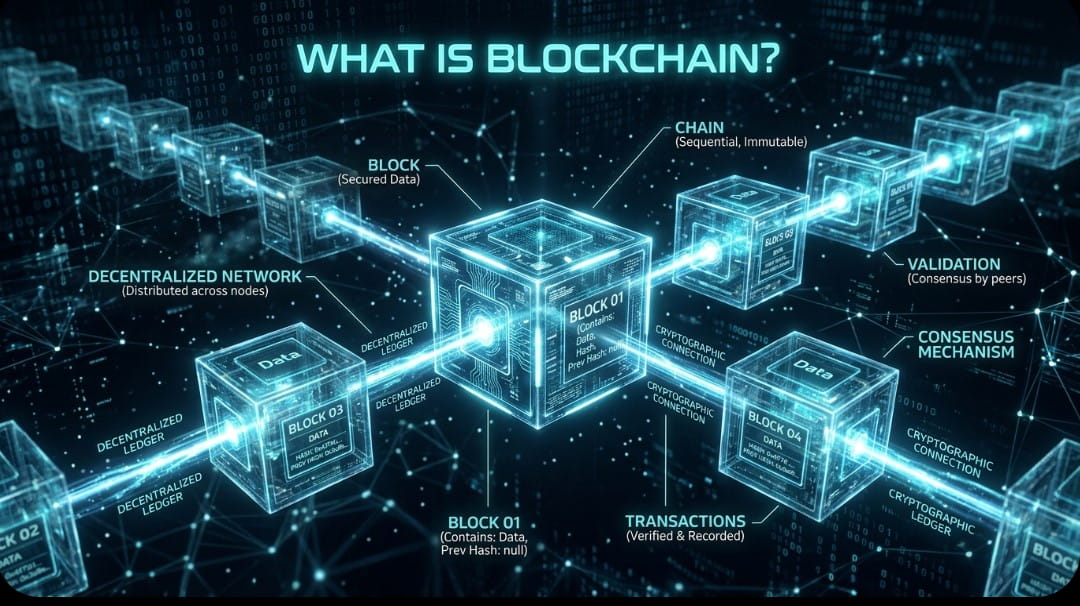

Unlike traditional databases that are controlled by a single institution, blockchain enables multiple trusted organizations to share synchronized records, automate business processes, strengthen audit trails, and improve transparency without sacrificing security. It is not a replacement for banks or financial institutions. Instead, it provides new infrastructure that can help financial organizations work together more efficiently while maintaining regulatory compliance.

Across the world, banks are exploring blockchain for cross-border payments and trade finance. Insurance companies are testing smart contracts to automate claims processing. Fintech firms are building faster payment solutions using distributed ledger technology. Governments are researching digital identity systems and central bank digital currencies. Cooperative societies are evaluating how blockchain could improve governance, member records, and loan management.

Kenya is part of this transformation.

As one of Africa’s leading fintech ecosystems, Kenya has built a reputation for innovation through mobile money, digital banking, and financial inclusion. Blockchain now represents another technology with the potential to reshape financial infrastructure across banks, SACCOs, insurance providers, fintech startups, payment companies, and government institutions.

This guide explains how blockchain is being applied across the financial services industry. The technical foundations of blockchain are covered in our What Is Blockchain? guide, this article explores practical applications, industry trends, opportunities, limitations, and what financial leaders should understand as blockchain adoption continues to evolve.

Whether you are a banker, SACCO executive, insurance professional, fintech founder, policymaker, regulator, researcher, or business owner, this article will help you understand where blockchain fits within modern financial services and where it is heading next.

Executive Summary

Blockchain is changing how financial institutions think about trust, collaboration, and record management. Instead of relying on separate databases maintained by individual organizations, blockchain enables multiple participants to work from the same verified version of financial information. This reduces duplication, strengthens audit trails, improves transparency, and supports more efficient business processes.

Financial institutions are exploring blockchain across a wide range of applications. Commercial banks are evaluating its use for cross-border payments, settlement, trade finance, fraud detection, and digital identity. Insurance companies are using blockchain to streamline claims processing and reduce fraud. SACCOs are examining how distributed ledgers can improve governance, member management, compliance, and loan administration. Fintech companies continue to build innovative payment systems, digital wallets, and embedded financial services using blockchain infrastructure.

While blockchain offers significant opportunities, it is not a universal solution. Successful adoption depends on choosing the right business problems, implementing appropriate governance, complying with regulations, and integrating blockchain with existing financial systems.

Let us examine how blockchain is being used throughout the financial services ecosystem, explores real-world applications, discusses emerging trends in Kenya and Africa, and provides a practical foundation for understanding the future of finance.

Quick Answer

How Is Blockchain Used in Financial Services?

Blockchain is used in financial services to securely share and verify financial records between trusted organizations. It supports faster payments, improves fraud prevention, strengthens compliance, simplifies auditing, enables digital identity verification, automates business processes through smart contracts, and reduces the need for manual reconciliation across banks, SACCOs, insurance companies, fintech firms, and payment providers.

Why Financial Services Need Blockchain

The financial sector has embraced digital transformation faster than almost any other industry.

Customers can now open bank accounts online, transfer money using mobile phones, apply for loans through apps, purchase insurance digitally, and invest without visiting a physical branch.

Behind these digital experiences, however, many financial institutions still rely on complex systems that were built decades ago. These systems often operate independently, requiring constant reconciliation, manual verification, and repeated exchange of information between organizations.

Blockchain has attracted attention because it addresses many of these longstanding operational challenges.

Duplicate Records

Every financial institution maintains its own records.

When two organizations exchange information, each keeps a separate copy. Over time, these records may differ because of delays, human error, or inconsistent updates.

This creates reconciliation work that consumes significant time and resources.

Blockchain provides a shared ledger where authorized participants work from the same verified information rather than maintaining separate versions.

Fraud

Financial fraud continues to evolve as digital financial services expand.

Common challenges include:

- Identity theft

- Document forgery

- Unauthorized account changes

- Duplicate transactions

- Internal fraud

- Payment manipulation

Blockchain creates permanent audit trails that make unauthorized changes easier to detect while strengthening accountability throughout financial processes.

It is important to recognize that blockchain reduces certain types of fraud but does not eliminate fraud altogether. Strong governance, cybersecurity, staff training, and internal controls remain essential.

Regulatory Compliance

Banks, SACCOs, insurers, and payment providers operate within highly regulated environments.

They must comply with requirements relating to:

- Anti-Money Laundering (AML)

- Know Your Customer (KYC)

- Financial reporting

- Record retention

- Risk management

- Consumer protection

- Data privacy

Meeting these obligations often requires collecting and verifying the same information multiple times.

Blockchain can simplify compliance by creating trusted, verifiable records that authorized parties can access when appropriate.

Cross-Border Delays

International payments frequently pass through several intermediary institutions before reaching their destination.

Each intermediary performs its own verification processes.

This increases:

- Processing time

- Operational costs

- Administrative complexity

Blockchain networks allow participating institutions to work from shared transaction records, reducing unnecessary duplication while improving transparency.

Manual Reconciliation

Financial institutions devote enormous resources to reconciling records between departments, branches, correspondent banks, payment providers, regulators, and business partners.

Manual reconciliation increases operational costs and introduces opportunities for human error.

Shared ledgers can significantly reduce this workload by ensuring all participants access synchronized information.

Identity Verification

Customers often repeat the same identity verification process whenever they interact with different financial institutions.

Opening a bank account, joining a SACCO, purchasing insurance, or applying for credit may require submitting identical documents several times.

Blockchain-based digital identity systems could enable customers to securely reuse verified credentials while maintaining greater control over their personal information.

Cybersecurity

As financial services become increasingly digital, cyber threats continue to grow.

Financial institutions invest heavily in:

- Network security

- Identity management

- Data encryption

- Fraud detection

- Incident response

Blockchain strengthens data integrity by making unauthorized modification of transaction histories extremely difficult while preserving complete audit trails.

Rising Operational Costs

Financial institutions face constant pressure to improve efficiency while maintaining high service standards.

Administrative costs continue to rise due to:

- Compliance obligations

- Legacy technology

- Manual processing

- Data reconciliation

- Security investments

Blockchain offers opportunities to streamline selected processes without compromising governance or regulatory oversight.

Legacy Infrastructure

Many financial organizations continue to operate systems developed years or even decades ago.

Replacing these systems entirely is often impractical.

Instead, blockchain is increasingly viewed as complementary infrastructure that connects existing systems rather than replacing them outright.

Quick Tip

Blockchain in financial services refers to the use of distributed ledger technology to improve trust, transparency, security, and operational efficiency across financial institutions while maintaining regulatory compliance.

The Financial Services Ecosystem

Financial services extend far beyond commercial banking.

The industry includes a diverse network of institutions that move money, manage risk, provide credit, facilitate investments, protect assets, and support economic growth.

Blockchain has potential applications across this entire ecosystem.

Commercial Banks

Commercial banks provide everyday financial services such as savings accounts, current accounts, loans, mortgages, payment services, and foreign exchange.

Blockchain may help banks improve:

- Payment processing

- Cross-border settlements

- Customer identity management

- Fraud detection

- Trade finance

- Regulatory reporting

Investment Banks

Investment banks facilitate large financial transactions involving governments, corporations, and institutional investors.

Potential blockchain applications include:

- Securities settlement

- Asset tokenization

- Syndicated lending

- Capital raising

- Custody services

SACCOs

Savings and Credit Cooperative Organizations play a critical role in financial inclusion, particularly across Kenya.

Blockchain may eventually support:

- Member records

- Loan administration

- Savings management

- Audit trails

- Governance

- Compliance

A dedicated article in this knowledge hub explores these applications in greater detail.

Further Reading: Blockchain for SACCOs: How Cooperative Societies Can Use Distributed Ledger Technology.

Microfinance Institutions

Microfinance organizations provide financial services to individuals and businesses that may not qualify for traditional banking.

Blockchain may strengthen:

- Digital identity

- Credit history

- Loan transparency

- Mobile lending

- Rural financial services

Compliance

Banks operate within one of the world’s most regulated industries.

Every customer account, transaction, loan, investment, and payment must comply with national and international regulations designed to protect consumers and maintain financial stability.

Key compliance requirements include:

- Know Your Customer (KYC)

- Anti-Money Laundering (AML)

- Counter-Terrorism Financing (CTF)

- Financial reporting

- Data protection

- Risk management

- Record retention

Meeting these obligations requires collecting, verifying, storing, and auditing enormous amounts of information.

Blockchain can simplify compliance by creating trusted records that authorized departments and regulators can verify without repeatedly requesting the same documentation.

Instead of replacing compliance processes, blockchain strengthens them through better transparency and more reliable audit trails.

Digital Identity

Customer onboarding remains one of banking’s most resource-intensive activities.

A customer opening multiple accounts with different institutions often repeats the same verification process several times.

This creates unnecessary friction for both customers and financial institutions.

Blockchain-supported digital identity systems could allow customers to securely reuse verified credentials while deciding exactly which information they wish to share.

For example, rather than uploading a national ID every time a new account is opened, a customer could grant permission for a verified digital credential to be used.

This approach offers several advantages:

- Faster onboarding

- Better customer experience

- Reduced identity fraud

- Lower compliance costs

- Stronger privacy controls

Digital identity is expected to become one of blockchain’s most significant long-term applications across financial services.

Cross-Border Banking

International banking has improved significantly over the past few decades, yet moving money across borders still involves multiple intermediaries.

Each institution performs its own verification procedures before forwarding transactions to the next participant.

This process increases:

- Processing time

- Administrative costs

- Settlement risk

- Operational complexity

Enterprise blockchain networks enable participating banks to exchange trusted transaction information directly while maintaining compliance with regulatory requirements.

Rather than replacing existing international payment infrastructure overnight, blockchain is increasingly being integrated into selected cross-border payment workflows where efficiency gains are greatest.

For African economies with growing regional trade and diaspora remittances, these improvements could have a significant long-term impact.

The Future of Banking

Banking is unlikely to become fully decentralized.

Instead, most experts expect the future to combine traditional banking with emerging technologies such as:

- Blockchain

- Artificial intelligence

- Cloud computing

- Open Banking

- Digital identity

- Real-time payments

- Automation

Banks already possess deep regulatory expertise, customer trust, capital strength, and extensive operational experience.

Blockchain adds another technology layer that can improve collaboration between institutions while maintaining regulatory oversight.

Future banking will likely focus less on replacing existing systems and more on connecting them more intelligently.

Further Reading: Blockchain in Banking: A Complete Guide to Enterprise Banking Transformation.

Blockchain for SACCOs

Savings and Credit Cooperative Organizations (SACCOs) occupy a unique position within Africa’s financial landscape.

Unlike commercial banks, SACCOs are member-owned institutions built on cooperation, shared responsibility, and community trust. Millions of people across Kenya rely on SACCOs for savings, affordable credit, investment opportunities, and financial empowerment.

As SACCOs continue their digital transformation, they face growing pressure to improve operational efficiency while maintaining transparency and member confidence.

Blockchain offers several opportunities to strengthen these objectives.

Member Management

Managing member information is one of every SACCO’s core responsibilities.

Records typically include:

- Membership details

- Savings contributions

- Loan history

- Guarantor relationships

- Dividend payments

- Voting rights

- Compliance records

Traditionally, these records are maintained within centralized databases.

Blockchain could provide a shared, tamper-evident ledger that preserves historical records while improving transparency and accountability.

Loan Administration

Loan management involves multiple stages:

- Application

- Assessment

- Approval

- Guarantor verification

- Disbursement

- Repayment

- Recovery

Every stage creates documentation and approval records.

Blockchain can strengthen these processes by maintaining an immutable audit trail that clearly shows who approved each stage and when those approvals occurred.

This improves accountability while simplifying future audits.

Savings Management

Savings contributions represent the foundation of most SACCO operations.

Members expect complete confidence that every contribution is accurately recorded.

Blockchain supports this expectation by maintaining transaction histories that are highly resistant to unauthorized modification.

This can strengthen member trust while reducing disputes relating to historical contribution records.

Governance

Good governance remains one of the strongest predictors of SACCO success.

Blockchain cannot create good governance, but it can strengthen governance practices by improving transparency around:

- Board resolutions

- Voting records

- Policy approvals

- Financial reporting

- Decision history

Leaders remain responsible for making sound decisions. Blockchain simply provides stronger evidence of how those decisions were made.

Audit and Compliance

Internal auditors, external auditors, and regulators require accurate financial records.

Blockchain simplifies auditing by preserving complete transaction histories that can be independently verified.

Instead of collecting records from multiple systems, auditors may access a synchronized history of approved transactions.

This can reduce audit preparation time while increasing confidence in reported information.

Transparency and Member Trust

Trust has always been central to cooperative finance.

Members contribute their savings because they believe their institution manages resources responsibly.

Blockchain reinforces this trust by making financial records more transparent, verifiable, and resistant to unauthorized changes.

It complements the cooperative principles upon which SACCOs were originally founded.

Further Reading: Blockchain for SACCOs: How Cooperative Societies Can Improve Transparency, Security, and Member Trust.

Blockchain in Insurance

Insurance depends on information.

Policies, premiums, customer identities, claims, assessments, and payments all require accurate records that multiple parties can trust.

Because insurers frequently exchange information with hospitals, repair centers, brokers, reinsurers, and regulators, blockchain offers opportunities to simplify collaboration while reducing fraud.

Claims Processing

Claims handling remains one of the industry’s most time-consuming processes.

A typical insurance claim may involve:

- Customer verification

- Policy validation

- Incident assessment

- Supporting documentation

- Payment approval

Blockchain enables authorized participants to access shared records, reducing duplication and improving transparency throughout the claims lifecycle.

Simple claims could eventually be processed much faster through smart contract automation.

Fraud Prevention

Insurance fraud costs the global industry billions of dollars every year.

Common examples include:

- Duplicate claims

- False documentation

- Identity fraud

- Inflated losses

- Multiple claims for the same incident

Blockchain strengthens fraud detection by creating permanent, verifiable histories of policies and claims.

Although it cannot eliminate fraudulent behavior, it makes inconsistencies easier to identify.

Policy Verification

Policy verification often requires insurers, brokers, healthcare providers, and customers to confirm identical information.

Blockchain provides a shared source of verified policy data, reducing delays while improving customer service.

Reinsurance

Large insurers frequently transfer portions of their risk to reinsurance companies.

These arrangements generate substantial administrative work involving documentation, premium calculations, and claims reconciliation.

Blockchain could improve efficiency by allowing insurers and reinsurers to work from synchronized records.

Digital Identity

Identity verification plays an increasingly important role in insurance underwriting and claims management.

Blockchain-supported digital identity could simplify onboarding while strengthening fraud prevention and customer privacy.

Smart Contracts

Smart contracts may eventually automate many routine insurance processes.

For example, predefined conditions could trigger automatic payments for straightforward claims once required verification has been completed.

Complex claims would still require human assessment, ensuring fairness and regulatory compliance.

Further Reading: Blockchain in Insurance: Transforming Claims, Fraud Prevention, and Digital Trust.

Blockchain in Microfinance

Microfinance institutions serve millions of individuals and small businesses that may not have access to conventional banking services.

Across Africa, they play a vital role in expanding financial inclusion, supporting entrepreneurship, and reducing poverty.

Blockchain has the potential to strengthen this mission by improving transparency, identity verification, and operational efficiency.

Financial Inclusion

Many underserved communities lack formal financial records despite maintaining active economic lives.

Blockchain-supported digital identities and transaction histories could help individuals build verifiable financial profiles, making it easier to access responsible financial services over time.

Small Business Lending

Small and medium-sized enterprises often struggle to demonstrate creditworthiness.

Blockchain-based financial records may provide more reliable evidence of business activity, improving lending decisions while reducing paperwork.

Mobile Lending

Mobile lending continues to expand rapidly across Africa.

Blockchain can support secure transaction records, automated repayments, and stronger customer identity management without changing the familiar mobile experience customers already use.

Rural Finance

Serving rural communities often involves operational challenges, including documentation, verification, and coordination between multiple service providers.

Blockchain may improve collaboration while preserving accurate financial records in distributed environments.

Blockchain in Fintech

Financial technology companies have transformed how people save, borrow, invest, insure, and transfer money. Unlike traditional financial institutions, fintech firms are often built around digital-first experiences, rapid innovation, and highly automated services.

Blockchain provides fintech companies with an infrastructure layer that supports secure data sharing, programmable transactions, and trusted digital interactions without relying entirely on centralized systems.

For many fintech companies, blockchain is not the product itself. Instead, it is an enabling technology that strengthens existing financial services.

Digital Wallets

Digital wallets have become an essential part of modern finance.

Consumers increasingly expect to store payment methods, transfer funds instantly, pay merchants, and manage financial services from their smartphones.

Blockchain can enhance digital wallets by supporting:

- Secure transaction histories

- Digital asset management

- Identity verification

- Cross-platform interoperability

- Lower settlement complexity

As digital payments continue to expand across Africa, blockchain-enabled wallet infrastructure may help improve efficiency while maintaining strong security standards.

Embedded Finance

Embedded finance refers to financial services integrated directly into non-financial platforms.

For example:

- Ride-hailing applications offering digital payments

- E-commerce platforms providing credit at checkout

- Agricultural marketplaces facilitating instant farmer payments

- Logistics platforms integrating insurance

Blockchain helps create trusted payment infrastructure behind these services while reducing the complexity of sharing information between multiple organizations.

Buy Now, Pay Later (BNPL)

Buy Now, Pay Later services have become increasingly popular in digital commerce.

These products require accurate customer identification, automated repayment schedules, and transparent financial records.

Blockchain can support BNPL providers through:

- Verified customer identities

- Transparent repayment records

- Smart contract automation

- Reduced disputes

Digital Lending

Many fintech companies specialize in digital lending.

Loan applications that previously required days or weeks can now be completed within minutes.

Blockchain strengthens these platforms by supporting:

- Trusted borrower records

- Digital identity

- Automated verification

- Secure loan histories

- Improved fraud detection

Artificial intelligence and blockchain together may eventually improve credit assessment while reducing operational risk.

Open Finance

Open Finance builds upon the ideas introduced by Open Banking.

Instead of keeping customer financial information isolated within individual institutions, customers can authorize secure sharing of selected financial data across approved service providers.

Blockchain provides an additional trust layer by improving transparency around data sharing and customer consent.

Financial APIs

Modern fintech ecosystems depend heavily on Application Programming Interfaces (APIs).

APIs allow banks, payment providers, insurers, and fintech companies to exchange information securely.

Blockchain complements API ecosystems by providing:

- Trusted transaction records

- Shared verification

- Secure interoperability

- Improved auditability

Rather than replacing APIs, blockchain strengthens the reliability of information exchanged between connected systems.

Further Reading: Blockchain in Fintech: How Distributed Ledger Technology Is Driving Financial Innovation.

Blockchain in Payment Systems

Payments are the foundation of every financial system.

Whether someone purchases groceries using a debit card, transfers money through mobile banking, pays school fees with mobile money, or sends funds internationally, payment systems ensure that money moves safely between individuals and organizations.

Although modern payment networks have become increasingly efficient, they still rely on multiple intermediaries, reconciliation processes, and independent verification systems.

Blockchain offers opportunities to simplify selected aspects of payment infrastructure.

Domestic Payments

Domestic payments generally involve banks, payment processors, merchants, clearing houses, and customers.

Each participant maintains separate transaction records.

Blockchain enables participating institutions to work from synchronized transaction histories, reducing duplicate reconciliation while improving transparency.

Potential benefits include:

- Faster settlement

- Lower operational costs

- Better payment visibility

- Improved fraud detection

- Reduced administrative overhead

International Payments

Cross-border payments remain significantly more complex than domestic transfers.

A single international payment may pass through several correspondent banks before reaching its destination.

Each intermediary introduces additional:

- Verification

- Processing time

- Transaction fees

- Operational complexity

Enterprise blockchain networks can reduce unnecessary duplication by enabling participating institutions to share verified transaction information directly.

Settlement

Settlement represents the final exchange of funds between financial institutions.

Traditional settlement may occur hours or days after a payment has been initiated.

Blockchain has the potential to reduce settlement times by maintaining synchronized records among participating institutions.

Near real-time settlement can improve liquidity while reducing operational risk.

Merchant Payments

Businesses increasingly expect payment systems that provide immediate confirmation and rapid settlement.

Blockchain infrastructure may support merchants by improving:

- Payment transparency

- Transaction tracking

- Automated reconciliation

- Customer confidence

This becomes particularly valuable for businesses processing large transaction volumes.

QR Code Payments

QR code payments continue expanding across Africa because they provide a simple and affordable payment experience.

Blockchain may strengthen QR payment ecosystems by supporting secure transaction verification and improved interoperability between payment providers.

Real-Time Payments

Consumers increasingly expect payments to happen immediately.

Waiting several days for settlement is becoming less acceptable in an increasingly digital economy.

Blockchain complements real-time payment initiatives by enabling faster verification and synchronized transaction records across participating institutions.

Mobile Money

Kenya’s mobile money ecosystem has become one of the world’s most recognized financial innovations.

Blockchain is unlikely to replace mobile money platforms.

Instead, it may strengthen them by supporting:

- Cross-network interoperability

- Improved settlement

- Enhanced fraud detection

- Better audit trails

- Regional payment connectivity

Central Bank Digital Currencies (CBDCs)

Central Bank Digital Currencies represent digital versions of national currencies issued by central banks.

Several countries are actively researching CBDCs as part of broader payment modernization initiatives.

Potential benefits include:

- Faster settlements

- Increased transparency

- Reduced payment costs

- Improved financial inclusion

- Better payment resilience

Not all CBDCs require blockchain, but distributed ledger technology remains one of the leading infrastructure options under consideration.

Comparison Table: Traditional Payments vs Blockchain-Enabled Payments

| Feature | Traditional Payments | Blockchain-Enabled Payments |

|---|---|---|

| Settlement | Often delayed | Potentially near real-time |

| Record Keeping | Separate institutional records | Shared synchronized ledger |

| Transparency | Limited between institutions | Greater transaction visibility |

| Reconciliation | Extensive manual processes | Reduced reconciliation |

| Cross-Border Processing | Multiple intermediaries | Fewer trusted participants |

| Audit Trail | Separate logs | Unified transaction history |

Blockchain for Cross-Border Payments

Cross-border payments represent one of blockchain’s most compelling financial applications.

Every year, individuals, businesses, governments, humanitarian organizations, and multinational corporations transfer trillions of dollars across international borders.

Despite advances in payment technology, international transfers often remain slower and more expensive than domestic payments.

Why Cross-Border Payments Are Complex

An international payment rarely moves directly from one bank to another.

Instead, it often passes through several intermediary institutions that perform:

- Identity verification

- Compliance screening

- Currency conversion

- Settlement

- Risk assessment

Every additional participant introduces cost and processing time.

Reducing Settlement Delays

Blockchain allows participating financial institutions to share trusted transaction records.

Instead of independently verifying the same information multiple times, institutions can rely on synchronized records while still meeting regulatory obligations.

This approach has the potential to significantly reduce settlement delays.

Lower Transaction Costs

Cross-border payments involve administrative expenses associated with reconciliation, compliance, messaging, and intermediary services.

By simplifying these workflows, blockchain may reduce operational costs while improving payment transparency.

Diaspora Remittances

Africa receives billions of dollars in remittances every year from citizens living and working abroad.

These funds support:

- Families

- Education

- Healthcare

- Small businesses

- Housing

- Community development

Lower-cost, faster remittance services could increase the value ultimately received by families.

Regional Trade

The African Continental Free Trade Area (AfCFTA) is expected to increase trade between African countries.

As cross-border commerce expands, businesses will require payment infrastructure that supports:

- Faster settlements

- Lower costs

- Trusted documentation

- Greater transparency

Blockchain may become an important component of future regional payment networks.

Blockchain for Trade Finance

Trade finance remains one of enterprise blockchain’s strongest commercial use cases.

International trade generates extensive documentation involving exporters, importers, shipping companies, customs authorities, logistics providers, insurers, and financial institutions.

Many of these records are still exchanged through fragmented systems.

Blockchain offers opportunities to improve collaboration across the supply chain.

Letters of Credit

Letters of credit provide payment guarantees between buyers and sellers.

Blockchain allows participating organizations to access synchronized documentation, reducing delays caused by manual verification.

Bills of Lading

Bills of lading confirm ownership and shipment of goods.

Recording these documents on blockchain reduces duplication while improving visibility across trading partners.

Import and Export Documentation

International trade often requires numerous approvals before goods can move across borders.

Blockchain simplifies document sharing while maintaining complete audit trails.

Supply Chain Finance

Businesses increasingly expect greater transparency throughout supply chains.

Blockchain enables trusted sharing of financial and logistical information among authorized participants, supporting faster financing decisions.

Blockchain in Capital Markets

Capital markets connect investors with businesses and governments seeking capital.

Although today’s markets are highly sophisticated, many post-trade activities remain operationally complex.

Blockchain has the potential to modernize several aspects of capital market infrastructure.

Securities Settlement

Traditional settlement involves exchanges, brokers, custodians, clearing houses, and financial institutions.

Blockchain enables synchronized ownership records that may reduce settlement times while improving transparency.

Digital Securities

Financial assets can increasingly be represented digitally.

Blockchain supports secure issuance, transfer, and management of these digital securities while maintaining verifiable ownership histories.

Custody

Institutional investors require secure custody solutions for financial assets.

Blockchain strengthens custody through cryptographic ownership verification and immutable transaction records.

Tokenization

Tokenization allows traditional assets such as shares, bonds, real estate, or investment funds to be represented digitally.

This could improve liquidity, increase market accessibility, and simplify ownership transfers.

Further Reading: Tokenization Explained: How Real-World Assets Are Becoming Digital.

Blockchain and Financial Inclusion

Financial inclusion means ensuring that individuals and businesses have access to affordable, useful, and responsible financial services.

These services include:

- Savings

- Credit

- Insurance

- Payments

- Investments

- Financial education

According to global development institutions, hundreds of millions of adults still lack access to formal financial services. Many people remain excluded because they cannot satisfy documentation requirements, live far from financial institutions, or operate within informal economies where traditional credit histories do not exist.

Across Africa, however, remarkable progress has been made through mobile money, digital banking, agency banking, and fintech innovation.

Blockchain is increasingly viewed as another technology that could help close the remaining gaps.

It is not a replacement for existing financial inclusion initiatives. Rather, it has the potential to strengthen them.

Serving the Unbanked

Many individuals who operate successful small businesses or earn consistent incomes still struggle to access formal financial services.

The problem is often not income.

It is the absence of trusted financial records.

Without documented transaction histories, lenders find it difficult to assess creditworthiness.

Blockchain can help create portable financial records that individuals control and can share with authorized institutions when seeking financial services.

This gives people an opportunity to demonstrate financial behaviour rather than relying solely on traditional documentation.

Supporting Small and Medium Enterprises (SMEs)

Small businesses are the backbone of many African economies.

Yet they frequently encounter obstacles when applying for financing because they cannot produce standardized financial records.

Blockchain-supported business records could improve transparency around:

- Business transactions

- Supplier payments

- Revenue history

- Loan repayment performance

These records may help lenders make more informed decisions while reducing paperwork for entrepreneurs.

Empowering Women Entrepreneurs

Across Africa, women continue to face barriers to accessing affordable finance despite making significant contributions to local economies.

Blockchain-supported digital identity and portable financial records may help reduce some of these barriers by strengthening documentation and improving access to formal financial systems.

Technology alone cannot eliminate inequality, but it can remove some of the administrative obstacles that disproportionately affect underserved communities.

Youth and Digital Finance

Africa has one of the world’s youngest populations.

Young entrepreneurs are increasingly comfortable using:

- Mobile banking

- Digital wallets

- E-commerce

- Mobile money

- Online investments

Blockchain complements this digital ecosystem by strengthening trust, security, and interoperability between financial services.

As digital economies expand, younger generations are likely to become major beneficiaries of blockchain-enabled financial infrastructure.

Rural Communities

Distance continues to limit access to traditional banking services in many regions.

Digital financial platforms have already reduced this barrier considerably.

Blockchain may further improve rural financial services by enabling secure collaboration between:

- Banks

- SACCOs

- Microfinance institutions

- Mobile money providers

- Government agencies

This creates opportunities for more efficient service delivery without requiring every institution to build duplicate systems.

Mobile Money and Financial Inclusion

Kenya demonstrated that financial inclusion can accelerate when technology addresses real community needs.

Mobile money transformed how millions of people save, borrow, receive salaries, pay bills, and send money.

Blockchain represents another layer of infrastructure that may strengthen future payment ecosystems by improving interoperability, transparency, and settlement efficiency.

Rather than replacing mobile money, blockchain can help connect multiple financial systems more effectively.

Cooperative Finance

Cooperative finance has long promoted financial inclusion by serving communities that traditional banking sometimes overlooks.

SACCOs understand local members, encourage savings, and provide affordable credit.

Blockchain aligns naturally with these principles because it strengthens transparency, accountability, and trust between members and their institutions.

This is why cooperative finance is widely viewed as one of blockchain’s most promising long-term applications.

Highlight:

Financial inclusion is not only about giving people access to financial services. It is about giving them access to trusted financial systems.

Blockchain for Digital Identity

Identity sits at the centre of every financial relationship.

Before opening an account, approving a loan, issuing insurance, processing investments, or completing a payment, financial institutions must verify who they are dealing with.

This process protects customers while helping institutions comply with regulatory requirements.

Yet identity verification remains one of the most repetitive, expensive, and frustrating parts of financial services.

The Problem with Current Identity Systems

Today, customers repeatedly submit the same information to different institutions.

A person may provide:

- National identification

- Passport

- Utility bill

- Passport photograph

- Tax information

- Employment details

The same documents may then be requested again by another bank, insurer, SACCO, investment platform, or payment provider.

This creates unnecessary duplication.

Self-Sovereign Identity

One of blockchain’s most promising concepts is Self-Sovereign Identity (SSI).

Instead of institutions permanently owning customer identity records, individuals securely control their own verified credentials.

When required, they grant permission for specific information to be shared.

For example, a customer could confirm that they are over eighteen years old without revealing their full date of birth.

Similarly, they could verify residence without exposing unrelated personal information.

This approach improves both privacy and efficiency.

Customer Onboarding

Digital identity can significantly simplify onboarding.

Instead of repeating lengthy verification procedures, customers could securely reuse previously verified credentials across participating financial institutions.

Potential benefits include:

- Faster account opening

- Better customer experience

- Lower administrative costs

- Reduced identity fraud

- Improved compliance

KYC and AML

Know Your Customer (KYC) and Anti-Money Laundering (AML) requirements remain essential to protecting the financial system.

Blockchain does not eliminate these obligations.

Instead, it can improve how institutions share verified identity information while maintaining appropriate customer consent and regulatory oversight.

This reduces duplication without reducing compliance standards.

Identity Fraud

Identity fraud remains one of the fastest-growing forms of financial crime.

Criminals increasingly exploit stolen identities to:

- Open fraudulent accounts

- Apply for loans

- Conduct money laundering

- Commit payment fraud

Blockchain-supported digital identities strengthen verification while making unauthorized identity changes easier to detect.

Privacy Considerations

Blockchain identity systems must balance transparency with privacy.

Financial institutions cannot expose sensitive customer information publicly.

Enterprise blockchain platforms therefore use permissioned access controls that ensure only authorized parties can view protected information.

Privacy remains one of the most important design principles in enterprise blockchain systems.

Blockchain and Regulatory Compliance

Regulation protects confidence in financial markets.

Customers deposit money because they trust financial institutions to operate responsibly under effective regulatory oversight.

Blockchain has the potential to make regulatory compliance more efficient without weakening governance.

Reporting

Financial institutions submit extensive reports to regulators.

These reports often require collecting information from multiple internal systems before submission.

Blockchain reduces this complexity by preserving synchronized financial records that authorized departments can access more efficiently.

Auditing

Audits consume considerable time because auditors must verify information from numerous independent systems.

Blockchain creates a chronological history of approved transactions, making audit preparation faster while strengthening confidence in reported information.

AML Monitoring

Money laundering remains a global challenge.

Blockchain provides stronger transaction visibility while supporting monitoring systems that identify suspicious financial activity.

However, effective AML programs still require human investigation, regulatory oversight, and advanced analytics.

KYC Management

Financial institutions frequently repeat customer verification procedures.

Blockchain enables secure sharing of verified customer credentials between authorized institutions, reducing administrative duplication while maintaining compliance.

Record Retention

Financial regulations often require organizations to preserve records for many years.

Blockchain supports long-term record integrity by maintaining tamper-evident transaction histories that remain available for future audits and investigations.

Data Integrity

Data integrity means information remains complete, accurate, and unaltered throughout its lifecycle.

Blockchain strengthens integrity through cryptographic verification and distributed record management.

This makes unauthorized modification significantly more difficult than in conventional systems.

RegTech and SupTech

Regulatory Technology (RegTech) helps financial institutions comply with regulations more efficiently.

Supervisory Technology (SupTech) helps regulators oversee financial institutions using advanced digital tools.

Blockchain complements both by providing trusted, verifiable data that improves reporting accuracy and regulatory visibility.

Blockchain Security

Security remains one of blockchain’s greatest strengths, but it is also one of the most misunderstood aspects of the technology.

Many people assume blockchain cannot be attacked.

That is incorrect.

Blockchain significantly improves data integrity, but complete security still depends on people, governance, software quality, cybersecurity controls, and operational discipline.

Cryptographic Protection

Every transaction is protected using cryptographic techniques that help verify authenticity and preserve integrity.

Rather than relying on trust alone, blockchain relies on mathematical verification.

Immutable Records

Once verified and added to the blockchain, records become extremely difficult to alter without detection.

This immutability strengthens:

- Financial reporting

- Compliance

- Auditing

- Governance

- Fraud investigations

Distributed Trust

Unlike centralized databases, blockchain distributes trust across multiple participating organizations.

This reduces dependence on a single point of control while improving resilience.

Fraud Prevention

Blockchain helps reduce opportunities for:

- Transaction manipulation

- Duplicate records

- Unauthorized modifications

- Hidden changes

However, it cannot prevent:

- Social engineering

- Insider threats

- Weak passwords

- Poor governance

- Human error

These risks still require comprehensive cybersecurity programs.

Security Limitations

Organizations considering blockchain should understand its limitations.

Blockchain cannot compensate for:

- Poor software development

- Weak access controls

- Inadequate governance

- Untrained staff

- Poor operational procedures

Technology strengthens security, but people remain essential.

Higlights

Blockchain creates stronger trust in data. It does not eliminate the need for strong governance, cybersecurity, or responsible leadership.

Smart Contracts in Financial Services

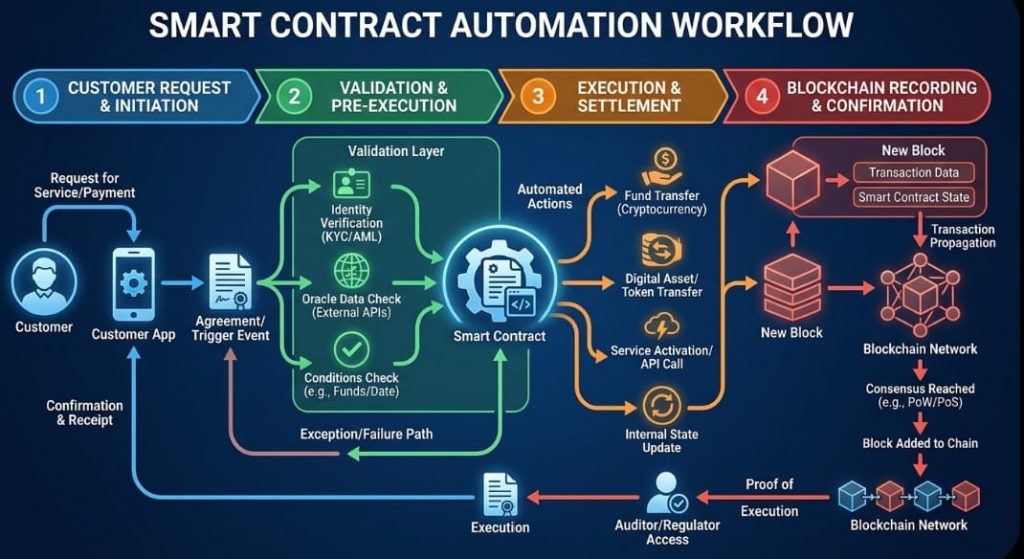

One of blockchain’s most transformative capabilities is the smart contract.

A smart contract is a computer program stored on a blockchain that automatically performs predefined actions when agreed conditions are met.

Unlike traditional contracts, which require people to manually verify conditions before taking action, smart contracts execute business rules consistently and transparently.

It is important to understand that a smart contract is not a replacement for legal agreements. Instead, it automates specific parts of a business process while remaining subject to applicable laws, regulations, and organizational governance.

For financial institutions, this creates opportunities to reduce repetitive administrative work while improving speed and accuracy.

Loan Automation

Traditional loan processing often involves several departments reviewing the same information.

A typical workflow includes:

- Customer application

- Identity verification

- Credit assessment

- Document validation

- Approval

- Disbursement

- Repayment monitoring

Many of these steps still involve manual processing.

Smart contracts can automate predefined stages once required conditions have been verified.

For example, a loan may automatically progress to the next approval stage once:

- Identity verification is complete

- Required documents are uploaded

- Credit criteria are satisfied

- Internal approvals are recorded

This reduces administrative delays while preserving oversight for higher-risk decisions.

Insurance Claims

Insurance companies process millions of claims every year.

Simple claims often involve repetitive verification before payment is approved.

Smart contracts can automate straightforward scenarios such as:

- Flight delay compensation

- Crop insurance

- Parametric weather insurance

- Shipment insurance

- Travel insurance

Once trusted data confirms that contractual conditions have been satisfied, payment instructions can be generated automatically.

More complex claims involving investigations or medical assessments would still require human review.

Payment Automation

Recurring financial activities can also benefit from smart contracts.

Examples include:

- Supplier payments

- Subscription billing

- Dividend distribution

- Loan repayments

- Scheduled settlements

Automation reduces manual intervention while improving consistency across financial operations.

Escrow Services

Escrow arrangements require funds to remain securely held until agreed conditions have been fulfilled.

Traditionally, this involves trusted third parties.

Smart contracts can automate escrow by releasing funds only after predefined contractual obligations have been satisfied.

Potential applications include:

- Property purchases

- International trade

- Business acquisitions

- Equipment leasing

Securities Settlement

Capital markets continue to explore smart contracts for post-trade settlement.

Ownership transfers, dividend payments, and corporate actions could be executed more efficiently through automated workflows while maintaining regulatory oversight.

Compliance Automation

Many compliance activities follow predefined rules.

Smart contracts can automatically:

- Record approvals

- Generate compliance alerts

- Validate transaction requirements

- Trigger reporting workflows

This allows compliance professionals to focus on higher-value investigations rather than repetitive administrative tasks.

Dividend Distribution

Banks, SACCOs, investment funds, and cooperatives regularly distribute dividends or profit shares.

Smart contracts can calculate and distribute these payments according to predefined rules while maintaining complete audit trails.

Smart Contract Workflow

Artificial Intelligence and Blockchain in Finance

Artificial intelligence and blockchain are often discussed together because they solve different parts of the same problem.

Artificial intelligence helps organizations make better decisions.

Blockchain helps organizations trust the information those decisions are based on.

Together, they create powerful opportunities for financial innovation.

Fraud Detection

Artificial intelligence excels at identifying unusual transaction patterns.

Blockchain provides reliable transaction histories.

Combining the two enables financial institutions to:

- Detect suspicious transactions earlier

- Reduce false positives

- Improve investigation accuracy

- Strengthen financial crime prevention

Credit Scoring

Traditional credit scoring often depends on limited financial histories.

Artificial intelligence can analyze broader datasets while blockchain provides trusted transaction records.

This combination may improve lending decisions, particularly for individuals and businesses with limited formal credit histories.

Intelligent Automation

Financial institutions increasingly automate repetitive work.

AI can classify documents, extract information, and identify anomalies.

Blockchain preserves trusted records of every automated decision.

This combination strengthens both efficiency and accountability.

Risk Analysis

Banks constantly evaluate financial risk.

Artificial intelligence identifies emerging patterns.

Blockchain ensures the underlying financial data remains accurate and verifiable.

Together they improve confidence in risk assessments.

Document Intelligence

Financial organizations process enormous volumes of documentation every day.

Artificial intelligence can automatically:

- Read contracts

- Extract financial information

- Classify documents

- Detect inconsistencies

Blockchain then provides an immutable audit trail showing when documents were received, approved, or modified.

Predictive Compliance

Future compliance systems may become increasingly proactive.

Artificial intelligence could identify compliance risks before they become regulatory issues.

Blockchain preserves trusted records supporting every compliance decision.

Quick Tip

Artificial intelligence predicts. Blockchain verifies. Together they create more intelligent and trustworthy financial systems.

Cloud Computing and Blockchain

Enterprise blockchain networks rarely operate on standalone servers.

Most organizations deploy blockchain infrastructure using cloud platforms because they provide scalability, reliability, security, and operational flexibility.

Cloud computing has therefore become one of blockchain’s most important enabling technologies.

Why Cloud Matters

Cloud platforms simplify blockchain deployment by providing:

- Secure infrastructure

- High availability

- Disaster recovery

- Backup services

- Monitoring tools

- Identity management

This allows financial institutions to focus on business applications rather than hardware maintenance.

Enterprise Blockchain Deployment

Most financial institutions do not build blockchain networks from scratch.

Instead, they deploy enterprise blockchain platforms through managed cloud environments.

This reduces implementation complexity while improving scalability.

Hybrid Cloud

Some organizations choose hybrid architectures.

Sensitive systems remain within private infrastructure while blockchain services operate across secure cloud environments.

This approach balances flexibility with regulatory requirements.

Multi-Cloud Strategies

Large financial institutions increasingly adopt multi-cloud environments to improve resilience and avoid dependence on a single provider.

Blockchain platforms can operate across multiple cloud providers while maintaining synchronized ledgers between participating organizations.

Enterprise Blockchain Platforms Used in Finance

Not every blockchain platform serves the same purpose.

Public cryptocurrency networks differ significantly from enterprise platforms designed for regulated financial institutions.

The following platforms are among the most widely discussed in enterprise finance.

| Platform | Best Suited For | Primary Strength |

|---|---|---|

| Hyperledger Fabric | Banks, insurers, enterprise networks | Permissioned collaboration |

| R3 Corda | Banking and financial institutions | Financial agreements and privacy |

| Hyperledger Besu | Enterprise blockchain | Flexible Ethereum compatibility |

| Quorum | Enterprise finance | Private transaction support |

| Ethereum | Public blockchain applications | Smart contracts and developer ecosystem |

| Stellar | Payments and remittances | Fast cross-border transactions |

| Ripple | Banking payments | International settlement networks |

Choosing the Right Platform

The correct platform depends on organizational requirements.

Factors include:

- Privacy requirements

- Regulatory obligations

- Transaction volume

- Governance model

- Integration needs

- Performance expectations

- Cost considerations

Most regulated financial institutions prefer permissioned enterprise platforms rather than fully public blockchain networks.

Public vs Private Blockchain

Selecting the appropriate blockchain architecture is one of the earliest strategic decisions an organization must make.

Comparison Table

| Feature | Public Blockchain | Private Blockchain |

|---|---|---|

| Access | Open to everyone | Authorized participants only |

| Governance | Decentralized community | Single organization or consortium |

| Privacy | Limited | High |

| Performance | Moderate | High |

| Regulatory Compliance | More difficult | Easier |

| Enterprise Suitability | Limited | Excellent |

| Banking Use | Rare | Common |

| SACCO Use | Limited | Strong candidate |

Which Is Better for Financial Services?

For most financial institutions, permissioned blockchain networks provide the best balance between:

- Privacy

- Performance

- Regulatory compliance

- Governance

- Security

This explains why enterprise banking initiatives frequently adopt private or consortium blockchain models.

Challenges of Blockchain Adoption in Financial Services

Blockchain offers significant opportunities, but successful implementation requires careful planning. Many organizations become excited by the technology itself and overlook the operational, regulatory, and organizational changes needed to realize measurable value.

Financial institutions should begin with clearly defined business problems rather than adopting blockchain simply because it is an emerging technology.

Scalability

Modern financial institutions process enormous transaction volumes.

Global payment networks handle thousands of transactions every second during peak periods.

Some blockchain networks were not originally designed for this scale.

Although enterprise blockchain platforms continue to improve performance, scalability remains an important consideration when selecting an implementation approach.

Organizations should evaluate:

- Expected transaction volumes

- Response time requirements

- Network growth projections

- Infrastructure capacity

Privacy

Financial institutions manage highly confidential customer information.

Unlike public cryptocurrency networks, enterprise finance requires strict privacy controls.

Organizations must ensure:

- Customer data remains confidential.

- Access is limited to authorized participants.

- National data protection laws are respected.

- Regulatory reporting requirements are maintained.

Permissioned blockchain networks address many of these concerns, but privacy must remain central to system design.

Integration with Existing Systems

Very few financial institutions are building entirely new infrastructures.

Instead, blockchain must integrate with existing technologies, including:

- Core banking systems

- Accounting software

- Enterprise Resource Planning (ERP)

- Customer Relationship Management (CRM)

- Mobile banking

- Payment gateways

- Mobile money platforms

- Regulatory reporting systems

Successful integration often represents a larger project than implementing the blockchain itself.

Regulation

Financial institutions operate in one of the world’s most regulated environments.

Before adopting blockchain, organizations must understand requirements relating to:

- Consumer protection

- Financial reporting

- Data privacy

- Cybersecurity

- Anti-Money Laundering

- Digital identity

- Cross-border transactions

As blockchain adoption grows, regulatory frameworks will continue evolving alongside the technology.

Skills and Talent

Blockchain combines expertise from multiple disciplines.

Successful projects require professionals with knowledge of:

- Software engineering

- Cryptography

- Cybersecurity

- Financial services

- Cloud computing

- Compliance

- Project management

The shortage of experienced blockchain professionals remains one of the industry’s biggest challenges.

Investment in education and workforce development will play a major role in future adoption.

Cost

Implementing enterprise blockchain involves more than purchasing software.

Organizations should consider:

- Infrastructure

- Development

- Integration

- Training

- Security

- Governance

- Maintenance

- Change management

Return on investment should always be evaluated against clearly defined business objectives.

Governance

Technology cannot compensate for weak governance.

Financial institutions still require:

- Clear policies

- Risk management

- Internal controls

- Ethical leadership

- Accountability

Blockchain strengthens governance by improving transparency, but leadership remains responsible for decision-making.

Interoperability

Financial institutions rarely operate independently.

Banks, insurers, SACCOs, payment providers, regulators, and fintech companies all exchange information.

Future blockchain success will depend on interoperability between different platforms and standards.

The greatest value will come from collaboration rather than isolated blockchain networks.

Hightlights:

Blockchain should never be adopted because it is fashionable. It should be adopted only when it solves a clearly defined business problem better than existing alternatives.

Blockchain Adoption in Kenya

Kenya has built one of Africa’s most innovative financial ecosystems.

From mobile money and agency banking to digital lending and fintech innovation, the country has consistently demonstrated an ability to adopt technologies that expand financial inclusion.

Blockchain now represents another area of growing interest.

Although large-scale enterprise adoption remains in its early stages, research, pilot projects, academic programs, and private sector investment continue to grow.

Central Bank of Kenya (CBK)

The Central Bank of Kenya continues to monitor developments in digital finance, payment innovation, and emerging technologies.

Like many central banks worldwide, CBK has shown interest in understanding blockchain’s implications for payment systems, financial stability, and digital currencies.

Future adoption will depend on regulatory priorities, technological maturity, and market readiness.

SASRA

The SACCO Societies Regulatory Authority oversees Kenya’s regulated SACCO sector.

As SACCOs continue their digital transformation, technologies that improve governance, transparency, record management, and compliance may become increasingly relevant.

Blockchain could eventually complement existing supervisory frameworks by strengthening auditability and record integrity.

Commercial Banks

Kenyan banks continue investing heavily in:

- Digital banking

- Artificial intelligence

- Cloud computing

- Automation

- Cybersecurity

Blockchain forms part of this broader digital transformation agenda, particularly in areas such as cross-border payments, trade finance, identity management, and fraud prevention.

Fintech Ecosystem

Kenya remains home to one of Africa’s most vibrant fintech communities.

Startups continue exploring blockchain across areas including:

- Payments

- Digital identity

- Agricultural finance

- Supply chains

- Asset tokenization

- Financial inclusion

Many innovations focus on solving practical local challenges rather than simply replicating international cryptocurrency products.

Insurance Industry

Kenya’s insurance sector continues embracing digital transformation through online services, mobile platforms, and data analytics.

Blockchain may further strengthen:

- Claims management

- Policy verification

- Fraud prevention

- Customer identity

Capital Markets

Capital market institutions continue evaluating technologies that improve transparency, settlement efficiency, and investor confidence.

Blockchain could contribute to future modernization initiatives involving digital securities and post-trade infrastructure.

Universities

Kenyan universities increasingly include blockchain within programs covering:

- Computer science

- Information systems

- Financial technology

- Cybersecurity

- Artificial intelligence

This investment in education will help develop the expertise needed for future enterprise adoption.

Innovation Hubs

Innovation hubs across Kenya continue supporting startups researching blockchain applications in finance, agriculture, healthcare, logistics, and public services.

These communities play an important role in transforming research into commercially viable solutions.

Kenya’s Digital Future

Kenya has repeatedly demonstrated that technology adoption succeeds when solutions address real social and economic needs.

Blockchain’s long-term success will depend on delivering measurable value rather than simply introducing new technology.

Blockchain Adoption Across Africa

Africa presents one of the world’s most exciting opportunities for blockchain innovation.

The continent combines rapid digital transformation with significant opportunities to improve financial inclusion, regional trade, and public services.

Nigeria

Nigeria has developed one of Africa’s largest fintech ecosystems.

Blockchain innovation continues across payments, remittances, digital identity, and financial technology.

South Africa

South Africa remains a regional leader in financial services innovation.

Banks, insurers, and technology companies continue exploring enterprise blockchain applications for financial markets and trade finance.

Rwanda

Rwanda continues investing heavily in digital government and technology-driven economic development.

Blockchain research aligns with the country’s broader digital transformation strategy.

Ghana

Ghana has expanded digital payment infrastructure while encouraging fintech innovation.

Blockchain continues attracting interest across financial services and public sector modernization.

Egypt

Egypt’s financial sector continues embracing digital banking, payment modernization, and fintech innovation.

Blockchain forms part of broader discussions surrounding financial technology and economic modernization.

AfCFTA

The African Continental Free Trade Area has the potential to reshape trade throughout Africa.

Greater regional commerce will require:

- Trusted documentation

- Efficient payments

- Secure digital identity

- Transparent financial systems

Blockchain could become an important supporting technology for this emerging continental economy.

Pan-African Payments

Cross-border payments remain one of Africa’s largest financial challenges.

Blockchain may complement regional payment initiatives by improving settlement efficiency and interoperability between participating institutions.

The Future of Blockchain in Financial Services

Blockchain is unlikely to replace existing financial systems.

Instead, it will increasingly become part of a broader technology ecosystem alongside artificial intelligence, cloud computing, automation, and digital identity.

Several trends are expected to shape the next decade.

Open Finance

Customers increasingly expect control over their financial information.

Open Finance enables secure data sharing across authorized service providers.

Blockchain strengthens trust, transparency, and consent management within these ecosystems.

Embedded Finance

Financial services will continue becoming integrated into everyday digital experiences.

Consumers may access lending, insurance, savings, and investments directly through retail, transport, agriculture, and healthcare platforms.

Blockchain provides trusted infrastructure supporting these interconnected services.

Artificial Intelligence

Artificial intelligence will increasingly automate:

- Risk assessment

- Fraud detection

- Customer service

- Compliance

- Financial forecasting

Blockchain ensures these systems operate using trusted, verifiable information.

Central Bank Digital Currencies

Research into Central Bank Digital Currencies is expected to continue.

While implementation timelines differ across countries, CBDCs represent one of the most closely watched developments in modern financial infrastructure.

Tokenization

Digital representation of traditional assets will likely expand.

Future tokenized assets may include:

- Government bonds

- Company shares

- Real estate

- Carbon credits

- Investment funds

Tokenization could improve liquidity while increasing access to investment opportunities.

Digital Identity

Digital identity is expected to become foundational to future financial services.

Trusted identity systems reduce fraud while improving customer experience across banks, insurers, SACCOs, fintech companies, and government services.

Real-Time Settlement

Customers increasingly expect immediate financial services.

Blockchain supports infrastructure capable of faster settlement, improved transparency, and reduced operational complexity.

Web3

Although still evolving, Web3 introduces concepts around decentralized digital ownership and programmable financial services.

Enterprise adoption will likely focus on practical business applications rather than speculation.

Programmable Money

Money itself may become increasingly programmable.

Future payment systems could automatically execute predefined business rules while remaining subject to legal and regulatory oversight.

Autonomous Finance

Combining blockchain, artificial intelligence, and automation may eventually enable financial systems that perform routine operations with minimal manual intervention.

Human oversight, however, will remain essential for governance, ethics, and regulatory accountability.

Frequently Asked Questions (FAQs)

1. What is blockchain in financial services?

Blockchain in financial services is the use of distributed ledger technology to securely record, verify, and share financial transactions among authorized participants. It helps banks, SACCOs, insurers, fintech companies, and payment providers improve transparency, reduce fraud, automate processes, and lower operational costs without relying solely on centralized databases.

2. How is blockchain used in banking?

Banks use blockchain to improve payment processing, cross-border transfers, trade finance, customer identity verification, fraud detection, regulatory compliance, and transaction settlement. Most banks use private or permissioned blockchain networks rather than public cryptocurrency blockchains because they provide greater privacy and regulatory control.

3. How can SACCOs use blockchain?

SACCOs can use blockchain to strengthen member record management, savings tracking, loan administration, governance, auditing, dividend distribution, and regulatory compliance. Blockchain creates an immutable record of financial activities, improving transparency and increasing member confidence.

4. Can blockchain replace traditional banks?

No. Blockchain is not designed to replace banks. Instead, it enhances banking operations by improving security, transparency, automation, and collaboration between financial institutions. Banks will continue to provide essential services such as lending, financial advice, risk management, and regulatory compliance.

5. What are the benefits of blockchain in financial services?

Some of the biggest benefits include:

- Faster transaction settlement

- Reduced fraud

- Improved transparency

- Better audit trails

- Lower reconciliation costs

- Stronger cybersecurity

- Enhanced regulatory compliance

- Improved customer identity management

- Greater operational efficiency

- Increased trust among participants

6. How does blockchain improve cross-border payments?

Blockchain enables participating financial institutions to share trusted transaction records instead of repeatedly verifying the same information. This can reduce settlement times, lower transaction costs, improve payment transparency, and make international money transfers more efficient.

7. Is blockchain secure for financial institutions?

Yes, blockchain is considered highly secure because it uses cryptography, distributed data storage, digital signatures, and tamper-evident records. However, blockchain is only one part of an organization’s security strategy. Financial institutions still require strong cybersecurity, governance, employee training, and access controls.

8. What is the difference between blockchain and traditional financial databases?

Traditional databases are typically managed by a single organization that controls updates and access. Blockchain distributes verified records across multiple authorized participants, making transactions more transparent, traceable, and resistant to unauthorized changes.

9. What is a smart contract in financial services?