Blockchain has become one of the most talked-about technologies of the past decade. It powers cryptocurrencies like Bitcoin, supports digital assets worth trillions of dollars, and is increasingly being adopted by governments, banks, logistics companies, healthcare providers, and financial institutions across the world.

Yet despite all the attention, blockchain remains widely misunderstood

This guide explains blockchain from the ground up. No technical background is required. Every concept is introduced in plain English, supported by practical examples and real-world applications. Along the way, you’ll also discover where blockchain fits, where it doesn’t, and why understanding it matters regardless of whether your organization ever deploys it.

Executive Summary

Blockchain is a digital record-keeping system that allows information to be shared securely across many computers instead of being stored in one central location. Every new record is verified by a network of participants before being permanently added to a growing chain of information. Once recorded, the information becomes extremely difficult to alter without everyone noticing.

This design creates transparency, improves data integrity, and reduces opportunities for fraud or unauthorized changes. Because every participant works from the same verified version of the records, blockchain can increase trust between organizations that may not fully trust each other.

Originally developed to support Bitcoin in 2009, blockchain has evolved into a broader technology platform used in finance, supply chain management, healthcare, government services, digital identity, and enterprise applications. Large organizations now use blockchain to improve efficiency, automate business processes through smart contracts, strengthen cybersecurity, and create reliable audit trails.

What is Blockchain?

Quick Tip

Blockchain is a secure digital ledger that records transactions across multiple computers rather than storing them in one central database. Every new transaction is verified by the network, grouped into blocks, and permanently linked to previous records using cryptography. This creates a transparent, tamper-resistant history that organizations can trust without relying on a single central authority.

Simple Definition

Blockchain is a shared digital record book where information is stored in chronological order and cannot easily be changed once it has been verified.

Instead of one organization controlling the records, multiple participants maintain identical copies. Whenever new information is added, everyone updates their copy simultaneously after confirming the information is valid.

Think of it as a notebook that hundreds of people own together. Every time someone writes on a new page, everyone receives the exact same update. No one can secretly erase or rewrite previous pages because everyone else already has identical copies.

Technical Definition

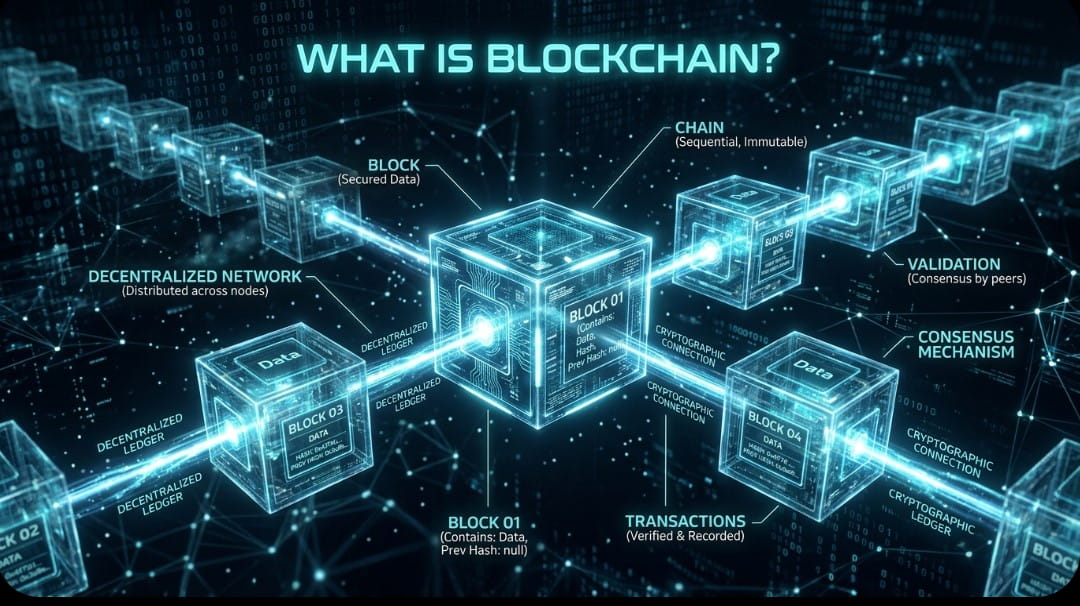

From a technical perspective, blockchain is a distributed ledger technology (DLT) that stores data in cryptographically linked blocks across a decentralized network of computers called nodes.

Each block contains:

- A collection of verified transactions

- A timestamp showing when the block was created

- A unique cryptographic hash

- The hash of the previous block

Because every block references the one before it, changing any historical information would require changing every subsequent block across the majority of participating computers. In most modern blockchain networks, this is computationally impractical.

Business Definition

For businesses, blockchain is a trusted system for sharing records between multiple organizations without requiring a single company to own or control the database.

Instead of reconciling different versions of financial records, contracts, inventories, or customer information, every participant works from one synchronized version of the truth.

This can reduce administrative work, improve transparency, strengthen compliance, and create faster audit processes.

Understanding Blockchain Through a Shared Ledger

Imagine a SACCO with five branch offices located in Nairobi, Nakuru, Kisumu, Eldoret, and Mombasa.

Every branch keeps a copy of the member savings register.

When Jane deposits KSh 20,000 at the Nairobi branch, every office immediately receives the updated balance after verifying the transaction.

No single branch owns the master record.

Everyone shares exactly the same information.

If someone attempted to secretly change Jane’s balance at one branch, the other four copies would immediately expose the inconsistency.

Blockchain works in much the same way, except computers automatically perform the verification, synchronization, and security checks using mathematics and cryptography rather than relying on manual reconciliation.

Quick Definition

Distributed Ledger: A database that is shared across many independent computers, ensuring every participant maintains the same verified version of the records.

History of Blockchain

Blockchain did not appear overnight. It is the result of decades of research in cryptography, computer science, distributed computing, and digital security.

Understanding this history helps explain why blockchain was designed the way it is today.

Early Foundations in Cryptography

Long before blockchain existed, researchers were exploring methods of protecting digital information through cryptography.

Cryptography is the science of securing information so that only authorized people can access or verify it.

During the 1970s and 1980s, important developments included:

- Public key cryptography

- Digital signatures

- Cryptographic hash functions

- Secure timestamping

These innovations later became essential building blocks for blockchain technology.

In 1991, researchers Stuart Haber and W. Scott Stornetta proposed a system for timestamping digital documents so they could not be altered after publication. Many experts consider this work one of blockchain’s earliest conceptual foundations.

Bitcoin Changes Everything

The modern blockchain era began in 2008 when an individual or group using the pseudonym Satoshi Nakamoto published the Bitcoin whitepaper titled Bitcoin: A Peer-to-Peer Electronic Cash System.

The paper introduced a revolutionary idea.

Instead of relying on banks to verify digital payments, thousands of independent computers could collectively agree on which transactions were valid.

In January 2009, the Bitcoin network went live, becoming the world’s first successful blockchain implementation.

Although Bitcoin introduced blockchain to the world, blockchain itself was always much broader than cryptocurrency.

Its real innovation was solving the long-standing challenge of establishing trust in digital transactions without requiring a central authority.

Ethereum’s Expansion

Bitcoin demonstrated that blockchain could securely record financial transactions without a central authority. However, developers soon realized that the same technology could do much more than move digital money.

In 2015, the Ethereum network introduced smart contracts, which are self-executing computer programs stored on a blockchain. These programs automatically perform predefined actions when certain conditions are met.

For example, imagine a SACCO loan application.

Instead of staff manually checking every requirement before releasing funds, a smart contract could automatically verify that:

- The member has met the minimum savings requirement.

- The guarantors have approved the loan.

- The loan falls within lending policies.

- Compliance checks have been completed.

If all conditions are satisfied, the loan approval process can proceed automatically without additional manual intervention.

This doesn’t eliminate human oversight. Rather, it automates repetitive processes while maintaining an auditable record of every action.

Today, Ethereum remains one of the world’s largest blockchain platforms and has inspired thousands of decentralized applications ranging from financial services to supply chain management.

Enterprise Blockchain

As blockchain matured, businesses began asking a different question.

Instead of allowing anyone in the world to participate, could blockchain be adapted for organizations where only approved participants should access the network?

This led to the development of enterprise blockchain platforms.

Unlike public blockchains, enterprise blockchain networks restrict participation to trusted organizations. They focus less on cryptocurrencies and more on securely sharing business information.

Some of the best-known enterprise blockchain platforms include:

- Hyperledger Fabric

- R3 Corda

- Quorum

- Hyperledger Besu

These platforms are now being used in industries such as:

- Banking

- Insurance

- Supply chain management

- Healthcare

- Manufacturing

- Government services

- Trade finance

Enterprise blockchain places greater emphasis on:

- Privacy

- Regulatory compliance

- Performance

- Governance

- Business process automation

How Blockchain Works

Blockchain works by collecting transactions, verifying them through a network of computers, grouping them into blocks, and permanently linking each new block to previous ones using cryptography.

Rather than trusting one central authority, participants collectively agree that each transaction is valid before it becomes part of the permanent record.

Although the technology behind blockchain can be sophisticated, its basic process is surprisingly straightforward.

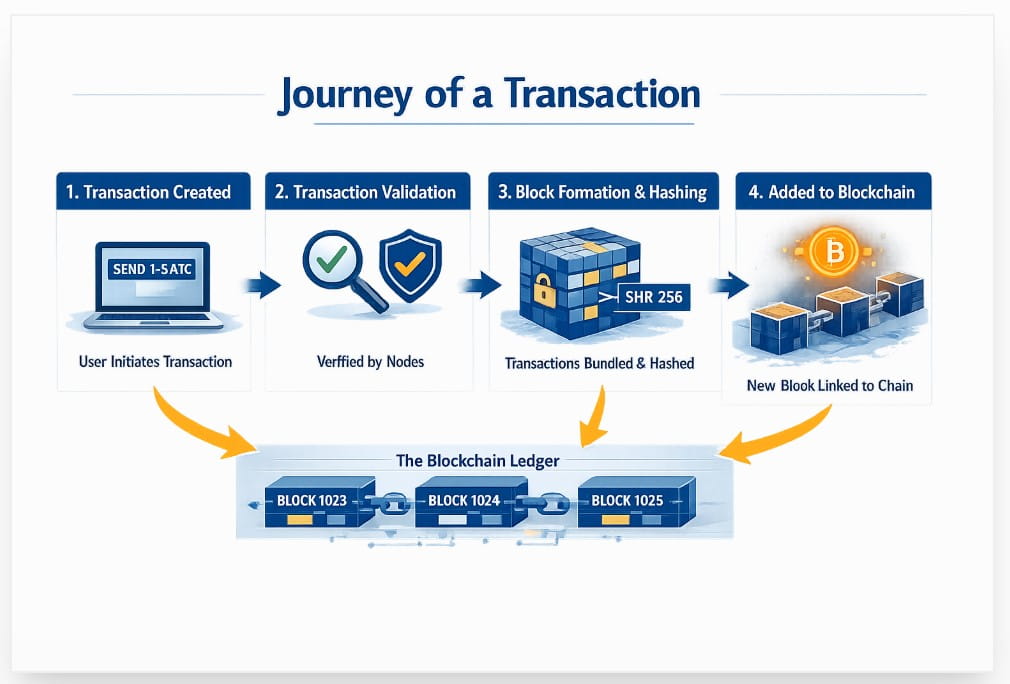

Step 1. A Transaction Is Created

Every blockchain process begins with an event.

That event could be:

- Sending money

- Recording a loan payment

- Updating ownership of an asset

- Registering a digital certificate

- Approving a business contract

Imagine Peter deposits KSh 15,000 into his SACCO savings account.

The system creates a transaction containing information such as:

- Sender

- Receiver

- Amount

- Time

- Digital signature

At this point, the transaction has been created but not yet confirmed.

Step 2. The Transaction Is Shared Across the Network

Instead of sending the transaction to one central database, it is broadcast to a network of computers known as nodes.

A node is simply a computer participating in the blockchain network.

Each node maintains a copy of the blockchain ledger.

Every participating computer receives the transaction and independently checks whether it appears legitimate.

Quick Tip

Node: A computer connected to a blockchain network that stores data, validates transactions, and helps maintain the integrity of the ledger.

Step 3. Validation Begins

The network now determines whether the transaction should be accepted.

Different blockchain systems use different validation methods known as consensus mechanisms.

Consensus simply means that the network reaches agreement before accepting new information.

Some common consensus methods include:

- Proof of Work

- Proof of Stake

- Practical Byzantine Fault Tolerance

- Proof of Authority

Enterprise blockchain platforms often use energy-efficient consensus models because participants are already known and trusted.

For example, a blockchain operated jointly by several SACCOs would not require anonymous participants to compete in solving mathematical puzzles as Bitcoin does.

Instead, designated validators could approve transactions much more efficiently.

Quick Tip

Consensus: The process through which blockchain participants collectively agree that a transaction is valid before adding it to the ledger.

Step 4. Verified Transactions Are Grouped into a Block

Once enough transactions have been verified, they are grouped together into a block.

A block is similar to a page in an accounting ledger.

Instead of storing just one transaction, a block may contain hundreds or even thousands of verified records.

Each block typically includes:

- Verified transactions

- Timestamp

- Previous block reference

- Cryptographic hash

- Additional network information

When the block is full, it becomes ready for permanent addition to the blockchain.

Quick Tip

Block: A collection of verified transactions that becomes part of the permanent blockchain record.

Step 5. Cryptographic Hashes Secure the Block

One of blockchain’s most important security features is the cryptographic hash.

A hash is a unique digital fingerprint created from the contents of a block.

Even changing a single letter or number inside the block produces an entirely different hash.

For example:

Original record:

Peter deposited KSh 15,000

Hash:

7dA93fB29XQ...

If someone secretly changed the amount to KSh 150,000, the hash would immediately become something completely different.

Because every block contains the hash of the previous block, changing one record would break the chain linking every subsequent block.

This is why blockchain records are considered tamper-evident.

Attempting to alter historical data would require recalculating every following block and convincing the majority of the network to accept those changes. On well-secured blockchain networks, this is extraordinarily difficult.

Quick Tip

Hash: A unique string of characters generated from data. Any change to the original data creates a completely different hash, making tampering immediately detectable.

Step 6. The Block Is Added to the Blockchain

Once validated, the new block is permanently attached to the previous block.

The chain now grows longer.

Block 1

│

▼

Block 2

│

▼

Block 3

│

▼

Block 4

│

▼

New Block

Each block references the one before it, creating a continuous chronological history.

This linked structure gives blockchain its name.

Step 7. Every Node Updates Its Copy

Finally, every participating computer updates its copy of the blockchain.

Instead of maintaining different versions of the records, everyone now shares exactly the same verified information.

This synchronization greatly reduces disputes caused by inconsistent databases.

For organizations that frequently exchange information, such as banks, SACCOs, insurers, regulators, and payment providers, working from one trusted version of the truth can significantly reduce reconciliation work.

Blockchain Process at a Glance

Types of Blockchain

Not all blockchains are designed the same way.

Some allow anyone to participate, while others restrict access to approved organizations. The right type depends on the goals of the organization, privacy requirements, regulatory obligations, and governance model.

The four main blockchain models are:

- Public blockchain

- Private blockchain

- Consortium blockchain

- Hybrid blockchain

1. Public Blockchain

A public blockchain is open to everyone.

Anyone can join the network, verify transactions, and view publicly available records.

Examples include:

- Bitcoin

- Ethereum

Advantages

- Highly decentralized

- Very transparent

- Resistant to censorship

- Large global community

- Strong security through distributed participation

Disadvantages

- Lower transaction speeds

- Higher energy use on some networks

- Public visibility of transaction history

- Limited privacy for organizations

Typical Use Cases

- Cryptocurrencies

- Public digital assets

- Open decentralized applications

- Global payment systems

2. Private Blockchain

A private blockchain is controlled by a single organization.

Only authorized participants can access the network.

This model offers greater control, faster performance, and stronger privacy, making it attractive for internal business operations.

Organizations can determine:

- Who joins the network

- Who validates transactions

- What information each participant can access

Private blockchains are commonly used for internal record management, enterprise workflows, and confidential business processes.

3. Consortium Blockchain

A consortium blockchain is jointly managed by multiple organizations rather than a single owner.

Instead of allowing anyone to participate, a group of trusted institutions governs the network together. Each member helps validate transactions and enforce agreed rules.

This model is particularly attractive for industries where organizations frequently exchange information but do not want one institution to control the entire system.

For example, several SACCOs, commercial banks, insurance companies, regulators, and payment service providers could operate a shared blockchain to exchange verified information securely while maintaining agreed governance standards.

Advantages

- Shared governance

- Improved trust between participating organizations

- Faster transactions than most public blockchains

- Better privacy controls

- Lower operating costs through collaboration

Disadvantages

- More complex governance

- Requires agreement among participating institutions

- Initial implementation can be time-consuming

Typical Use Cases

- Banking consortia

- Trade finance

- Healthcare information sharing

- Government agencies

- Cooperative financial ecosystems

4. Hybrid Blockchain

A hybrid blockchain combines features of both public and private blockchains.

Some information remains publicly visible for transparency, while sensitive information stays private and accessible only to authorized participants.

This approach gives organizations flexibility while maintaining regulatory compliance.

For instance, a SACCO could publicly verify that a loan agreement exists without revealing confidential member information.

Advantages

- Flexible privacy controls

- Greater scalability

- Better regulatory compliance

- Controlled transparency

- Supports multiple business models

Disadvantages

- More complex architecture

- Higher implementation costs

- Requires careful governance design

Typical Use Cases

- Government registries

- Healthcare

- Financial services

- Supply chain management

- Digital identity platforms

Comparison of Blockchain Types

| Feature | Public | Private | Consortium | Hybrid |

|---|---|---|---|---|

| Anyone can join | ✅ | ❌ | ❌ | Partial |

| Transparency | High | Low | Medium | Configurable |

| Transaction speed | Moderate | High | High | High |

| Privacy | Limited | Excellent | Good | Excellent |

| Governance | Community | Single organization | Multiple organizations | Shared |

| Best suited for | Cryptocurrencies | Internal business | Industry collaboration | Mixed environments |

Key Takeaway

Most SACCOs, banks, and regulated financial institutions would likely benefit more from private or consortium blockchain models than public blockchain networks.

Key Characteristics of Blockchain

Blockchain possesses several unique characteristics that distinguish it from conventional information systems. These characteristics work together to create secure, transparent, and trustworthy digital records.

Transparency

Every authorized participant can view the same version of the data.

Public blockchain networks allow anyone to inspect transactions, while enterprise blockchains restrict visibility based on permissions.

Transparency reduces disagreements because participants work from one consistent source of information.

Example

Instead of different branches maintaining slightly different financial records, every authorized office accesses the same verified ledger.

Security

Blockchain uses advanced cryptographic techniques to secure information.

Every transaction is digitally signed, verified by multiple participants, and linked to previous records through cryptographic hashes.

Because attackers would need to compromise multiple independent systems simultaneously, blockchain is generally more resistant to unauthorized modification than centralized databases.

It is important to note that blockchain does not eliminate cyber risk.

Poor application design, stolen passwords, weak governance, and compromised devices can still lead to security incidents.

Immutability

One of blockchain’s defining characteristics is immutability.

Once information has been validated and permanently recorded, changing it becomes extremely difficult.

This creates reliable historical records.

For financial institutions, immutable records simplify:

- Auditing

- Regulatory reporting

- Financial reconciliation

- Fraud investigations

- Compliance monitoring

Immutability does not necessarily mean information can never change.

If corrections are required, blockchain records those corrections as new transactions rather than deleting historical information.

This preserves the complete audit trail.

Decentralization

Traditional systems usually rely on one central authority.

Blockchain distributes responsibility among multiple participants.

No single computer owns the entire network.

This reduces dependence on one organization and improves resilience against system failures.

Traceability

Every transaction has a complete history.

Users can see:

- When it occurred

- Who authorized it

- Which records changed

- Previous transaction history

This makes blockchain especially valuable for industries where provenance matters.

Examples include:

- Agriculture

- Food safety

- Pharmaceutical products

- Supply chains

- Financial services

Automation

Many blockchain platforms support smart contracts.

Smart contracts automatically execute predefined business rules.

Examples include:

- Releasing payments

- Approving transactions

- Updating ownership records

- Issuing certificates

- Triggering compliance checks

Automation reduces manual processing while improving consistency.

Trust

Blockchain creates what many experts call digital trust.

Instead of relying entirely on one institution, participants trust the verification process itself.

This does not eliminate the need for governance, regulation, or oversight.

Rather, it provides stronger evidence that recorded information has not been altered improperly.

Resilience

Since multiple copies of the blockchain exist across the network, losing one computer does not destroy the records.

The network continues operating even if several nodes fail.

This makes blockchain more resilient than systems relying on a single database server.

Blockchain vs Traditional Databases

Many people assume blockchain is simply another database.

While blockchain does store information, its design philosophy is very different from conventional database systems.

Traditional databases prioritize speed, flexibility, and centralized management.

Blockchain prioritizes trust, integrity, transparency, and shared verification.

Detailed Comparison

| Feature | Traditional Database | Blockchain |

|---|---|---|

| Ownership | Single organization | Shared among participants |

| Data storage | Centralized | Distributed |

| Record modification | Can be edited | New records added while preserving history |

| Audit trail | May require separate logging | Built into the system |

| Trust model | Central authority | Network consensus |

| Transparency | Limited | Configurable depending on network type |

| Data integrity | Administrator controlled | Cryptographically verified |

| Fault tolerance | Depends on backups | Multiple synchronized copies |

| Security | Centralized controls | Cryptography and distributed validation |

| Performance | Very fast | Usually slower due to verification |

| Governance | Internal | Shared rules and protocols |

| Best suited for | Internal applications | Multi-party collaboration |

When Is a Traditional Database Better?

Blockchain is not the answer to every technology challenge.

A traditional database is often the better choice when:

- One organization fully owns the data.

- Very high transaction speed is required.

- Data changes frequently.

- Historical immutability is unnecessary.

- There is already sufficient trust among participants.

Examples include:

- Human resource systems

- Internal inventory databases

- Email platforms

- Customer relationship management systems

When Does Blockchain Make Sense?

Blockchain becomes valuable when multiple independent organizations need to:

- Share data securely

- Reduce reconciliation work

- Improve transparency

- Strengthen audit trails

- Prevent unauthorized record changes

- Establish trust without relying on a single central authority

Examples include:

- Banking networks

- Cross-border payments

- Cooperative societies

- Government registries

- Supply chains

- Digital identity ecosystems

Quick Tip

Blockchain should not replace every database. The most successful implementations solve specific trust and collaboration challenges rather than simply replacing existing technology.

Why Blockchain Matters

Blockchain matters because it addresses one of the oldest challenges in information management.

How can multiple organizations trust shared information without depending entirely on one central authority?

For decades, businesses have spent enormous resources reconciling records, resolving discrepancies, verifying transactions, and conducting audits.

Blockchain introduces a different model where participants share one synchronized, verifiable source of truth.

This shift has implications across many industries.

For Businesses

Businesses use blockchain to:

- Improve operational efficiency

- Reduce reconciliation costs

- Automate repetitive workflows

- Strengthen cybersecurity

- Increase transparency

- Simplify auditing

Large multinational companies are already experimenting with blockchain to improve procurement, logistics, digital identity, and contract management.

For Banks

Banks face constant pressure to process transactions faster while maintaining security and regulatory compliance.

Blockchain offers opportunities to improve:

- Cross-border payments

- Trade finance

- Settlement processes

- Fraud detection

- Customer identity verification

- Regulatory reporting

Many central banks are also researching blockchain as part of broader digital currency initiatives.

For Governments

Governments are exploring blockchain to improve public services and reduce administrative inefficiencies.

Potential applications include:

- Land registries

- Digital identity

- Public procurement

- Tax administration

- Business registration

- Voting systems

- Public record management

By creating tamper-evident records, blockchain can strengthen public confidence in government-managed information.

For Healthcare

Healthcare organizations manage enormous amounts of sensitive information. Patient records, prescriptions, laboratory results, insurance claims, and treatment histories all need to be accurate, secure, and accessible to authorized professionals.

Blockchain can help by creating a shared, tamper-evident record of medical information while allowing patients greater control over who accesses their data.

Potential applications include:

- Electronic health records

- Medical supply chain tracking

- Prescription verification

- Insurance claims processing

- Professional licensing

- Clinical research

It is important to note that blockchain is unlikely to replace existing hospital information systems. Instead, it can complement them by improving interoperability and strengthening trust between healthcare providers.

For Supply Chains

Supply chains involve many independent organizations, including manufacturers, transport companies, warehouses, wholesalers, retailers, regulators, and customers.

Each participant typically maintains separate records.

Blockchain creates a shared history of a product’s journey from origin to destination.

This improves:

- Product traceability

- Inventory visibility

- Counterfeit prevention

- Food safety

- Regulatory compliance

- Consumer confidence

Relatable Kenyan Example

Imagine a coffee cooperative in Nyeri exporting premium coffee beans to Europe.

Using blockchain, buyers could verify:

- Which farm produced the coffee

- Harvest date

- Processing location

- Export approvals

- Shipping milestones

- Sustainability certifications

Consumers scanning a QR code could view the verified history of the product before purchasing it.

For Education

Educational institutions issue millions of certificates every year.

Unfortunately, fake academic credentials remain a challenge in many countries.

Blockchain allows universities to issue digital certificates that employers can verify instantly without contacting the issuing institution.

Possible applications include:

- Academic certificates

- Professional licenses

- Skills credentials

- Research publications

- Student transcripts

Several universities around the world have already begun issuing blockchain-verified diplomas.

For Agriculture

Agriculture remains one of Africa’s largest economic sectors.

Blockchain has the potential to strengthen agricultural value chains by improving transparency from farm to market.

Applications include:

- Produce traceability

- Farmer identity verification

- Cooperative record management

- Input distribution

- Digital payments

- Crop insurance

- Carbon credit verification

For agricultural SACCOs and cooperatives, these innovations may eventually improve market access while reducing fraud and administrative costs.

For Insurance

Insurance depends heavily on trust and accurate information.

Blockchain can simplify many insurance processes by providing verified records that multiple parties can access securely.

Potential benefits include:

- Faster claims processing

- Fraud detection

- Automated payouts

- Policy verification

- Shared customer records

- Improved compliance

For example, crop insurance payouts could be triggered automatically when trusted weather data confirms that rainfall fell below agreed thresholds.

For Real Estate

Property transactions often involve multiple stakeholders, including buyers, sellers, banks, lawyers, surveyors, and government agencies.

Blockchain could improve transparency by creating secure digital property records.

Potential applications include:

- Land registries

- Property ownership verification

- Mortgage documentation

- Lease management

- Property transfers

Several governments are exploring blockchain-based land management systems to reduce fraud and improve public confidence.

Blockchain in Financial Services

Financial services involve the movement, storage, lending, investment, and protection of money.

Blockchain introduces new ways of managing financial information while improving transparency, security, and efficiency.

Rather than replacing existing financial institutions, blockchain is increasingly being used to enhance existing systems.

Payments

Traditional international payments often involve several intermediaries.

Each institution verifies information independently before forwarding funds to the next participant.

This process can increase costs and extend settlement times.

Blockchain networks allow participants to share a synchronized ledger, reducing duplicate verification and improving transaction visibility.

Potential benefits include:

- Faster settlements

- Lower processing costs

- Improved transparency

- Reduced reconciliation work

- Better tracking of payment status

Lending

Lending depends on accurate information about borrowers.

Blockchain could support lending by securely recording:

- Loan applications

- Credit history

- Collateral records

- Repayment history

- Guarantor approvals

Financial institutions could access verified records more efficiently, reducing administrative delays.

It is important to remember that blockchain does not replace credit assessment.

Institutions must still evaluate affordability, risk, and regulatory requirements.

Regulatory Compliance

Financial institutions operate under strict regulatory frameworks.

Compliance activities often include:

- Customer identification

- Transaction monitoring

- Record retention

- Audit reporting

- Anti-money laundering checks

Blockchain can simplify compliance by maintaining permanent, verifiable records that auditors and regulators can review when appropriate.

This reduces duplication while improving confidence in reported information.

Cross-Border Transactions

International payments often pass through several correspondent banks before reaching the recipient.

Each intermediary performs separate verification.

Blockchain can streamline this process by allowing participating institutions to work from the same verified transaction history.

Potential advantages include:

- Faster international settlements

- Improved transparency

- Lower operational costs

- Better payment tracking

These improvements are particularly relevant for Africa, where remittance costs remain among the highest globally.

Fraud Prevention

Fraud remains one of the financial sector’s greatest challenges.

Examples include:

- Identity theft

- Duplicate payments

- Document forgery

- Unauthorized record changes

- Insider manipulation

Blockchain helps reduce certain forms of fraud by making unauthorized changes easier to detect.

Every transaction creates a permanent audit trail.

This does not eliminate fraud entirely.

Fraudsters may still exploit human error, social engineering, stolen credentials, or weaknesses in applications connected to the blockchain.

Strong governance remains essential.

Digital Identity

Identity verification is fundamental to financial services.

Banks and SACCOs must confirm that customers are who they claim to be.

Blockchain-based digital identity systems could allow individuals to control verified identity credentials while deciding which organizations may access them.

Potential benefits include:

- Faster customer onboarding

- Reduced document duplication

- Improved privacy

- Stronger security

- Better compliance with Know Your Customer (KYC) requirements

Digital identity remains one of the fastest-growing areas of blockchain innovation worldwide.

Blockchain cannot solve these issues on its own.

Successful digital transformation requires people, policies, governance, technology, and continuous improvement working together.

Blockchain Adoption in Kenya

Kenya has earned international recognition as one of Africa’s leading technology and financial innovation hubs. The success of mobile money, digital banking, and fintech has created an environment where emerging technologies such as blockchain are attracting increasing interest.

While large-scale blockchain deployment is still developing, activity is growing across government, academia, startups, and the private sector.

Government Initiatives

The Government of Kenya has identified digital transformation as a national priority through various ICT and innovation strategies. While blockchain is still at an early stage of public sector adoption, government agencies continue to explore its potential in areas such as digital identity, land administration, public records, and secure data management.

As blockchain technologies mature, future applications could include:

- Land registry modernization

- Digital certificates

- Public procurement transparency

- Government record management

- Cross-agency data sharing

Like many countries, Kenya is taking a measured approach by balancing innovation with regulatory oversight.

Financial Institutions

Kenya’s financial sector has long been recognized as one of Africa’s most innovative.

Commercial banks, fintech companies, payment providers, and digital lenders continue to monitor blockchain developments, particularly in:

- Cross-border payments

- Trade finance

- Fraud detection

- Digital identity

- Asset tokenization

- Regulatory technology (RegTech)

While most financial institutions are not replacing their core banking systems with blockchain, many are evaluating how distributed ledger technology can improve specific business processes.

Universities and Research Institutions

Kenyan universities are increasingly introducing blockchain into courses covering:

- Computer science

- Cybersecurity

- Financial technology

- Information systems

- Artificial intelligence

- Software engineering

Research continues to grow around blockchain’s role in financial inclusion, governance, agriculture, healthcare, and public administration.

This academic investment is helping prepare the next generation of blockchain developers, researchers, policymakers, and entrepreneurs.

Innovation Hubs

Kenya’s innovation ecosystem has played an important role in blockchain experimentation.

Technology hubs, startup incubators, and fintech communities continue to explore blockchain applications in areas such as:

- Agriculture

- Supply chains

- Healthcare

- Digital identity

- Carbon markets

- Cooperative finance

- Financial inclusion

Many startups are focusing on solving local problems rather than simply replicating cryptocurrency products developed elsewhere.

Opportunities for Kenya

Blockchain presents several long-term opportunities for the Kenyan economy.

These include:

- Improved financial inclusion

- Stronger digital identity systems

- Better public record management

- More transparent supply chains

- Increased investor confidence

- Improved trade documentation

- Greater efficiency in financial services

- Enhanced cybersecurity

Challenges Facing Adoption in Kenya

Despite growing interest, several barriers remain.

These include:

- Limited technical expertise

- High implementation costs

- Regulatory uncertainty

- Limited public awareness

- Integration with legacy systems

- Shortage of blockchain professionals

- Infrastructure disparities between urban and rural areas

Successful adoption will require collaboration between government, regulators, universities, industry, and financial institutions.

Challenges of Blockchain

Blockchain offers significant potential, but it is not without limitations.

Understanding these challenges helps organizations make balanced technology decisions.

Scalability

As blockchain networks grow, processing every transaction across multiple participants can reduce performance.

Some blockchain networks process far fewer transactions per second than conventional payment systems.

Developers continue working on scalability improvements through technologies such as layer-two networks, sharding, and optimized consensus mechanisms.

Energy Consumption

Early blockchain networks such as Bitcoin became known for their high energy consumption because of the Proof of Work consensus mechanism.

Many modern blockchain platforms now use more energy-efficient alternatives such as Proof of Stake or enterprise consensus models.

As a result, energy consumption varies significantly depending on the blockchain platform being used.

Regulation

Blockchain continues to evolve faster than regulatory frameworks in many countries.

Key regulatory questions include:

- Consumer protection

- Data privacy

- Taxation

- Digital assets

- Cross-border transactions

- Anti-money laundering compliance

Clear regulation provides greater certainty for businesses considering blockchain investments.

Skills Shortage

Blockchain development requires expertise across multiple disciplines, including:

- Software engineering

- Cybersecurity

- Cryptography

- Networking

- Financial systems

- Governance

Demand for qualified professionals currently exceeds supply in many markets.

Investment in education and workforce development remains essential.

Implementation Costs

Deploying blockchain involves more than purchasing software.

Organizations may need to invest in:

- Infrastructure

- Staff training

- Process redesign

- Integration with existing systems

- Cybersecurity

- Governance frameworks

- Change management

For many organizations, implementation costs can outweigh the benefits if blockchain is applied to the wrong business problem.

Public Perception

Public understanding of blockchain is often shaped by news about cryptocurrency volatility or investment scams.

While cryptocurrencies use blockchain, the technology itself has many enterprise applications unrelated to digital currencies.

Improving digital literacy will help organizations evaluate blockchain based on practical business value rather than speculation.

Future of Blockchain

Artificial Intelligence

Artificial intelligence (AI) and blockchain can complement one another.

AI analyzes information and makes predictions.

Blockchain provides trusted, verifiable data.

Together they may support:

- Fraud detection

- Automated compliance

- Financial risk analysis

- Supply chain optimization

- Predictive maintenance

Smart Contracts

Smart contracts are expected to become increasingly sophisticated.

Future smart contracts may automate:

- Loan approvals

- Insurance claims

- Procurement

- Licensing

- Regulatory reporting

- Cooperative governance

Human oversight will remain essential for complex decision-making.

Digital Identity

Trusted digital identities may become one of blockchain’s most impactful applications.

Individuals could securely control verified credentials while sharing only the information required for specific transactions.

This approach could improve privacy while simplifying customer onboarding across financial services.

Central Bank Digital Currencies (CBDCs)

Many central banks are researching Central Bank Digital Currencies.

A CBDC is a digital form of national currency issued by a country’s central bank.

Not every CBDC uses blockchain, but distributed ledger technology is one option under consideration in several jurisdictions.

CBDCs could improve payment efficiency while supporting financial inclusion.

Tokenization

Tokenization refers to representing real-world assets digitally.

Examples include:

- Property

- Government bonds

- Company shares

- Carbon credits

- Commodities

- Art

Tokenization may improve liquidity and expand investment opportunities.

Web3

Web3 describes a vision of a more decentralized internet where users have greater control over digital assets and online identities.

Blockchain serves as one of the foundational technologies supporting many Web3 applications.

Although Web3 continues to evolve, many concepts remain experimental.

Financial Inclusion

Across Africa, blockchain may contribute to greater financial inclusion by supporting:

- Lower-cost remittances

- Digital identity

- Cross-border payments

- Cooperative finance

- SME financing

- Agricultural value chains

Technology alone, however, cannot solve financial exclusion.

Success also depends on infrastructure, regulation, affordability, education, and consumer trust.

African Innovation

Africa’s rapidly growing digital economy creates opportunities for locally developed blockchain solutions.

Rather than copying international models, African innovators are increasingly designing solutions around local priorities such as:

- Agriculture

- Cooperative finance

- Informal businesses

- Mobile payments

- Land administration

- Youth employment

Frequently Asked Questions

1. What is blockchain in simple terms?

Blockchain is a shared digital ledger that securely records information across multiple computers, making it very difficult to alter past records without network agreement.

2. Is blockchain the same as Bitcoin?

No. Bitcoin is a cryptocurrency that uses blockchain technology. Blockchain can also support many applications beyond digital currencies.

3. What is distributed ledger technology?

Distributed Ledger Technology (DLT) is a system where multiple participants maintain synchronized copies of the same records instead of relying on one central database.

4. Why is blockchain considered secure?

Blockchain uses cryptography, distributed validation, and immutable records to make unauthorized changes highly detectable.

5. Can blockchain be hacked?

The blockchain itself is extremely difficult to compromise, but applications, user accounts, or connected systems may still be vulnerable if poorly secured.

6. Does blockchain replace banks?

No. Blockchain complements many banking services but does not eliminate the need for regulated financial institutions.

7. What industries use blockchain?

Finance, healthcare, agriculture, logistics, insurance, government, education, manufacturing, and real estate all explore blockchain applications.

8. Is blockchain legal in Kenya?

Blockchain technology itself is legal. Organizations must still comply with applicable financial, data protection, and regulatory requirements.

9. What is a smart contract?

A smart contract is software stored on a blockchain that automatically executes agreed rules when predefined conditions are met.

10. Is blockchain environmentally harmful?

Some blockchain networks consume significant energy, while many modern platforms use highly energy-efficient consensus mechanisms.

11. What is the difference between blockchain and a database?

Traditional databases are centrally controlled. Blockchain distributes trust across multiple participants while preserving an immutable history.

12. Can blockchain prevent fraud?

Blockchain reduces opportunities for certain types of fraud but cannot eliminate fraud caused by human behavior or weak governance.

13. What is tokenization?

Tokenization converts ownership of real-world assets into secure digital representations that can be recorded on blockchain networks.

Glossary

- Blockchain: A distributed digital ledger that securely records transactions.

- Distributed Ledger: A database shared across multiple participants.

- Node: A computer participating in a blockchain network.

- Block: A collection of verified transactions.

- Hash: A cryptographic fingerprint representing data.

- Consensus: The process of agreeing that transactions are valid.

- Cryptography: Mathematics used to protect digital information.

- Smart Contract: Software that executes agreed rules automatically.

- Bitcoin: The first cryptocurrency built on blockchain.

- Ethereum: A blockchain platform supporting smart contracts.

- Private Blockchain: A blockchain restricted to authorized participants.

- Public Blockchain: A blockchain open to anyone.

- Consortium Blockchain: A blockchain governed by multiple organizations.

- Hybrid Blockchain: A blockchain combining public and private features.

- Immutable: Extremely difficult to alter after recording.

- Digital Identity: Verified electronic proof of identity.

- Tokenization: Digital representation of physical or financial assets.

- KYC (Know Your Customer): Identity verification required by financial institutions.

- AML (Anti-Money Laundering): Measures designed to prevent financial crime.

- Web3: A vision for a decentralized internet supported by blockchain technologies.

Conclusion

Blockchain is far more than the technology behind cryptocurrencies. It represents a different approach to recording, verifying, and sharing information among multiple participants. By combining cryptography, distributed ledgers, and consensus mechanisms, blockchain creates records that are transparent, resilient, and difficult to alter.

As Kenya and the rest of Africa continue their digital transformation, blockchain is likely to play a growing role alongside artificial intelligence, cloud computing, and modern financial technologies. Organizations that invest time in understanding these technologies today will be better prepared to evaluate tomorrow’s opportunities with confidence.

For this kind of news and more, visit us at MUIAA Ltd where we offer research, advice and build modern day innovations in blockchain, fintech, and digital finance across emerging markets. We help turn ground-level realities into practical financial tools.